Welcome to the last Credit Tip Tuesday of 2020! Today we are going to debunk the myth that checking your credit score affects your credit, explain the difference between a hard inquiry and a soft inquiry, and how to mitigate the impact on your credit score as much as possible.

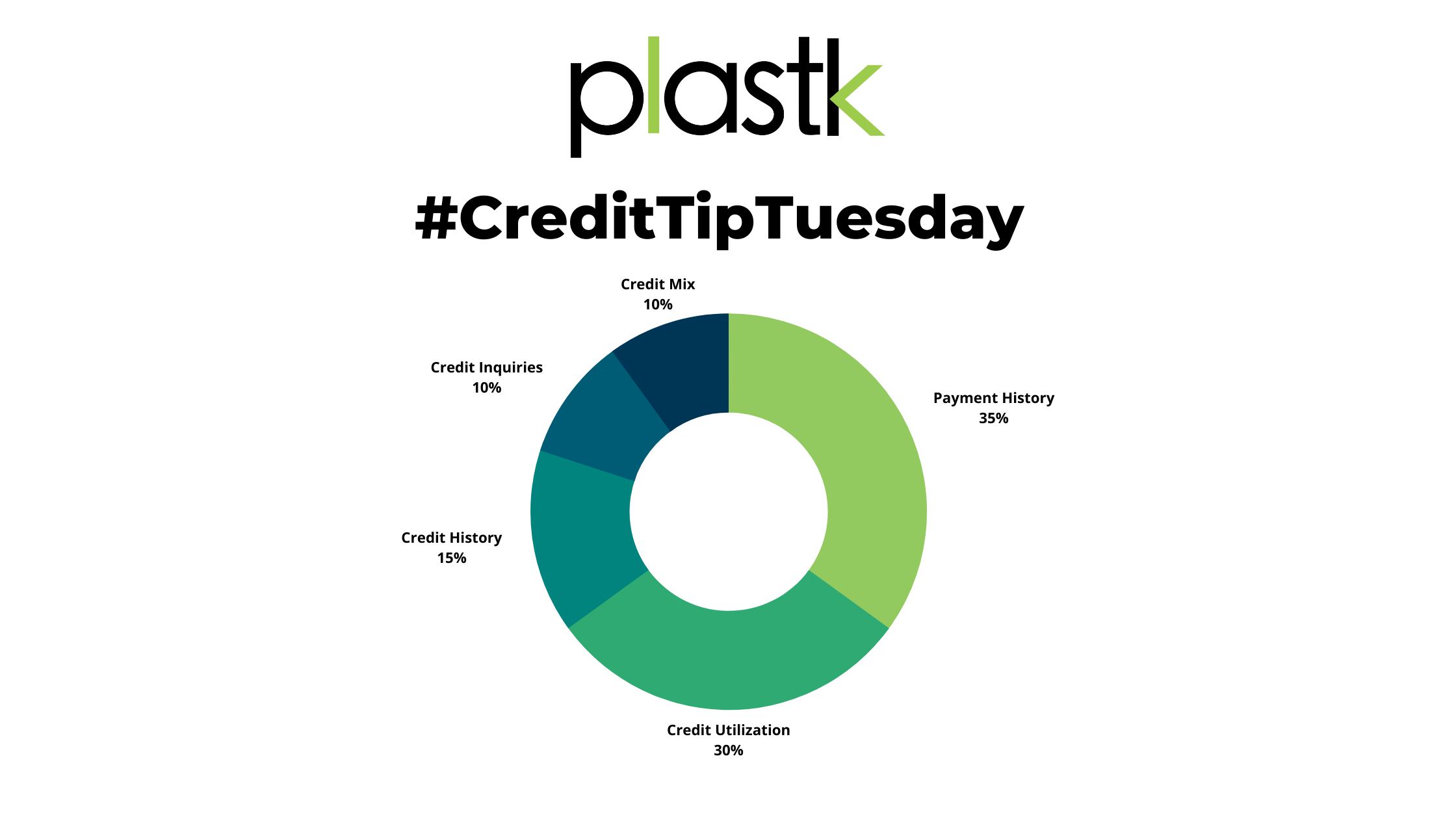

For the past few weeks we have been informing you about the 5 major things that affect your credit, if you remember them it's your payment history, credit utilization, credit history, credit mix, and last but not least credit inquiries. Although credit inquires only makeup about 10% of your score it is still important to know about it and what it does to your score.

There is a common misconception that every time you check your credit score you are lowering it, the reason for this is because many people are thinking about hard inquiries. Most times, when you pull your credit report this is a soft inquiry that does not impact your credit, in fact, knowing your credit is the easiest way to build it.

So what's the difference between a hard inquiry and a soft inquiry?

A soft inquiry is when you are just checking your credit report yourself (when there's no lending decision involved, you're just checking for your own knowledge) or if a lender is checking it for information but not to lend you credit.

Common examples of soft credit inquiries are:

- An employer doing a background check

- Checking your credit on the Plastk App or cardholder portal

- Applying for insurance

- Getting pre-qualified for certain credit cards

A hard inquiry is basically when a lender or credit card issuer requests to check your credit report as part of the loan application process. This will show up on your credit report that your credit was checked and according to Equifax, it may stay there for about 36 months and will only lower your score by a few points.

Common examples of hard credit inquiries are:

- Mortgage applications

- Auto loans

- Credit Cards

- Student loans

- Personal loans

- Apartment rental applications

Although one or two hard inquiries won't affect your score too much having multiple hard inquiries at the same time or within a couple of months may come off as a red flag for lenders as it seems like you are short on cash and applying for a lot of credit which means more debt and in turn making you "higher risk". So if you apply for multiple credit cards in one day, apply for a mortgage at a couple of different banks the next week and apply to finance a car at a few dealerships to see where you can get a better deal the following week, this will all be shown on your credit report and might look suspicious to lenders.

Combine your inquiries to mitigate the impact it has on your score:

Certain types of loans, like mortgage loans, bunch together your inquiries if they are for the same purpose within a specific period of time. The timeframes vary but it can range from 14 to 45 days. All of the inquiries will show on your report (for accuracy) but only one will affect your credit. For example, if you apply for a mortgage at 6 different institutions in 2 weeks all 6 times will show on your credit report but it counts as 1 "hard inquiry". Keep in mind that this is only for certain types of loans and does not apply to credit cards

Tips for mitigating the impact on your score:

- Find out if the type of loan you're applying for can be combined into one hard inquiry, if yes, make sure that you are aware of the time frame

- Check your credit report before getting quotes so you can understand what shows up on a report. You can see your credit report on our app when you upgrade to Plastk Sentinel.

- Don't apply for loans just to see if you qualify, only apply when you need the credit so it's worth it.

If you are looking around for the best deal on your mortgage or car loan, don't cut your shopping short because you are worried about affecting your credit score. In most cases, the impact that the hard inquiries have on your credit scores from shopping around will most likely be minimal compared to the benefits that you will get from finding a loan with a lower interest rate.

Knowledge is power so the more informed you are about what is on your credit report the better you can prepare for it. So now you know the five main factors that affect your credit and how you can use them to build your credit! If you haven't read about the other factors I encourage you to check out the other blogs as each factor works together to build your credit. Remember this is a process, you will not build your credit overnight but putting in good habits now will set you on the right path for the future. See you in 2021!

Disclaimer: The content provided on the Plastk Financial Inc. Blog is information to help Canadians become financially literate and learn about credit. Plastk is not responsible for building or ruining an individual's credit score or credit rating. It is neither tax nor legal advice, is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Tax, investment, credit inquiries, and all other decisions should be made, as appropriate, only with guidance from a qualified professional.